2026 Tax Shift: Your Charitable Giving Still Matters—But the Deduction Might Not - as much as Before.

Understand the 2026 charitable tax deduction changes under Public Law 119-21. Learn how standard vs. itemized filers are affected with real income examples.

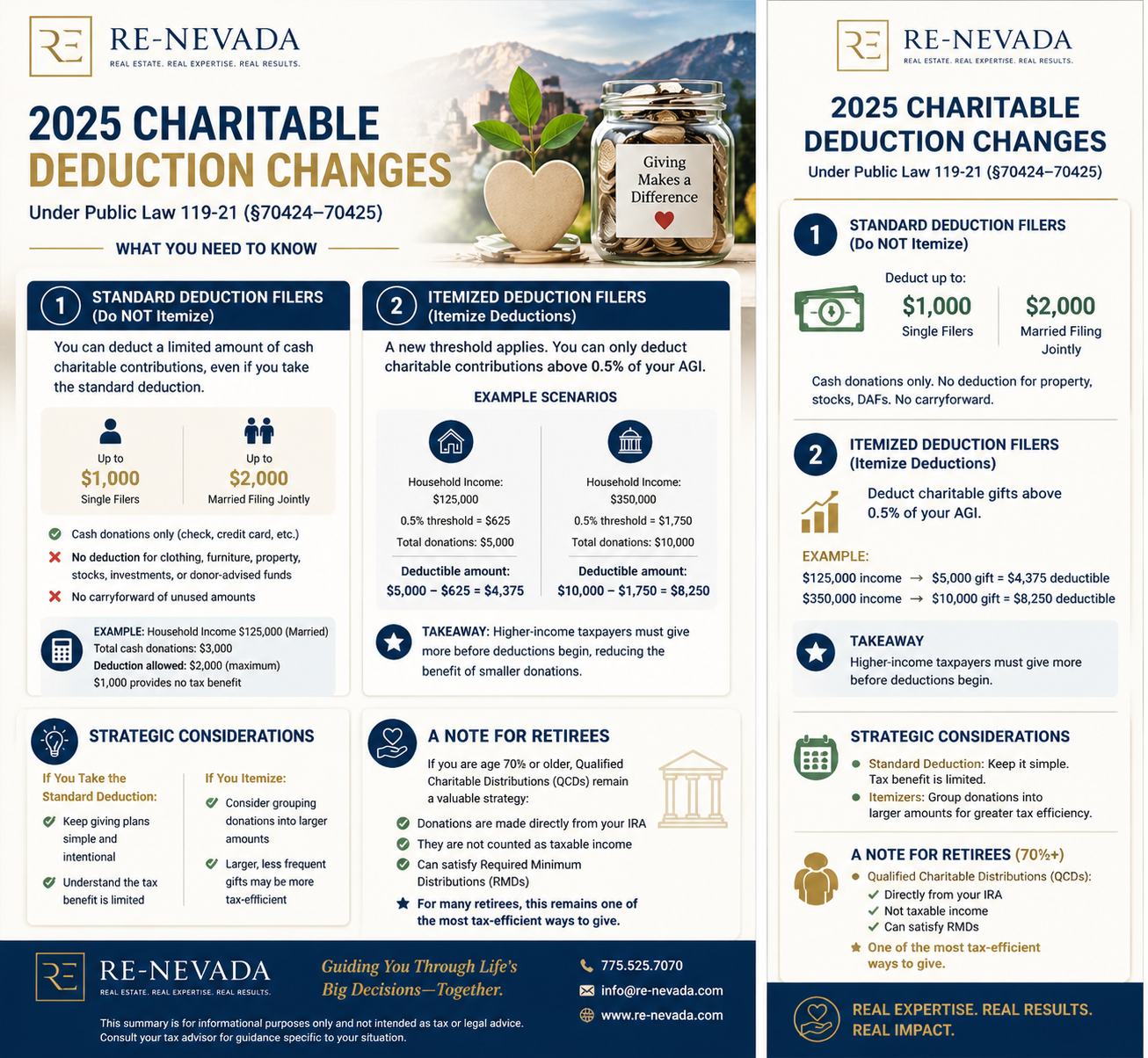

New Charitable Donation Tax Rules (Starting 2026)- New federal rules will change how charitable donations are deducted. These changes come from Public Law 119-21 (July 4, 2025) — specifically Sections 70424 and 70425 — and they affect taxpayers differently depending on how you file your taxes.

Understanding the Two Types of Tax Filers - Your strategy depends on whether you: Take the standard deduction (most taxpayers), or Itemize deductions (typically higher-income or more complex filings). Let’s break it down clearly:

For most taxpayers who take the standard deductionand do not itemize, a limited charitable deduction is now available: up to $1,000 for single filers and up to $2,000 for married couples filing jointly. However, this deduction applies only to cash contributions (such as those made by check or credit card) and does not include donations of clothing, furniture, other property, stocks, investments, or contributions to donor-advised funds. In addition, any unused portion cannot be carried forward to future tax years. For example, a married household earning $125,000 that donates $3,000 in cash can only deduct $2,000, with the remaining $1,000 providing no tax benefit. The key takeaway is that for standard deduction filers, the tax advantage of charitable giving is capped regardless of total contributions.

💼 Household Income: $125,000 (Married)

Total donations: $3,000 (cash)

Deduction allowed: $2,000 (maximum)

$1,000 provides no tax benefit

For taxpayers who itemize deductions, the rules are more nuanced. Under Section 70425, charitable contributions are only deductible to the extent they exceed 0.5% of adjusted gross income (AGI), meaning a portion of every donation is effectively non-deductible. For example, a household earning $125,000 must exceed a $625 threshold, so a $5,000 donation results in a deductible amount of $4,375. Similarly, a household earning $350,000 faces a $1,750 threshold, leaving $8,250 deductible on a $10,000 contribution. The key takeaway is that higher-income taxpayers must contribute more before receiving any tax benefit, which reduces the impact of smaller charitable donations.

💼 Household Income: $350,000

0.5% threshold = $1,750

Total donations: $10,000

Deductible amount:

$10,000 – $1,750 = $8,250

Strategic Considerations

When planning charitable giving, strategy matters depending on how you file. For those taking the standard deduction, it may be best to keep giving plans simple and intentional, recognizing that the associated tax benefit is limited regardless of contribution size. For those who itemize, a more strategic approach may be beneficial, such as grouping donations into larger amounts, since making fewer but larger contributions can be more tax-efficient under the current rules.

A Note for Retirees

For retirees age 70½ or older, Qualified Charitable Distributions (QCDs) continue to offer a highly effective giving strategy. These donations are made directly from an IRA, are not included as taxable income, and can be used to satisfy Required Minimum Distributions (RMDs). For many retirees, this remains one of the most tax-efficient ways to support charitable causes.

In conclusion, the changes under Public Law 119-21 (§70424–70425) doesn’t eliminate the benefits of charitable giving—but they do change how and when it makes sense from a tax perspective.

DISCLOSURE: This article is provided for general informational and educational purposes onlyand is not intended as legal, financial, or real estate advice. Information provided is for general informational purposes only, reflects the author’s opinion, may change without notice, and should be independently verified. This is not legal, financial, or real estate advice. Readers should consult appropriate professionals regarding their specific circumstances. As always consult regarding financial & tax related issue your legal counsel, CPA, and financial investment advisors

📌 About Us

At Real Estate In Nevada LLC, we believe informed clients make better decisions—whether in real estate, investing, or long-term financial planning.